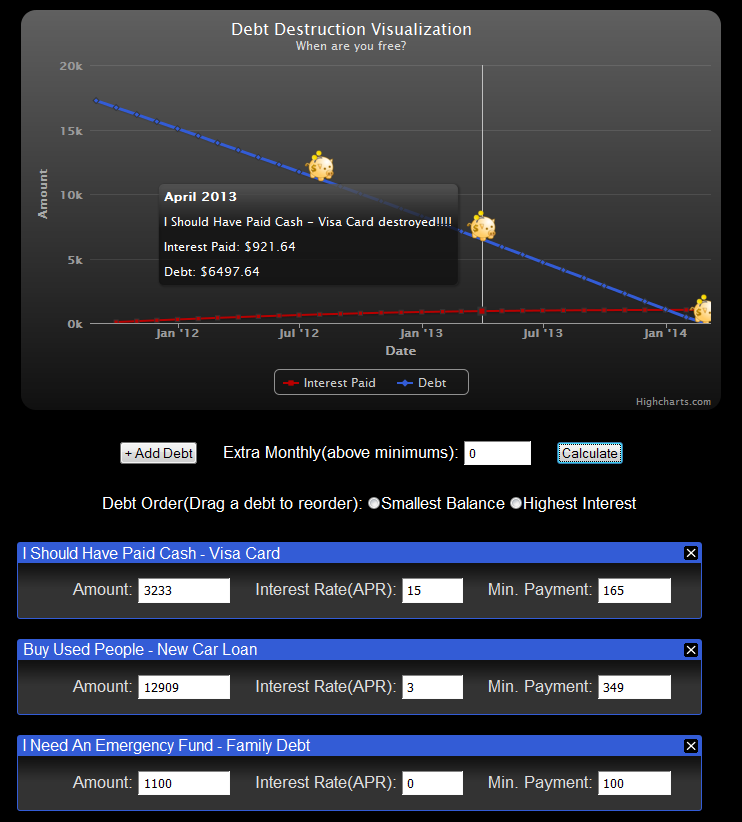

An alpha version is ready of the debt reduction calculator is ready. We will be adding features as the feedback rolls in, so feel free to check it out and leave some suggestions by clicking the “Feedback” tab. The calculator does...

With mortgage interest rates at amazing lows, I (Ed) figured now is the time for 15 year fixed rate refinance: I have a 30 year fixed rate mortgage with about 23 years and ~$156,000 left. With the 15 year fixed...

The following is a guest post by a dear friend and colleague Ed who is just months away from finally getting out from under $40,000+ in debt. Give him a warm welcome in the comments or a shout on twitter(@ed_bruner): The...

Tonight at dinner I told me wife that we were down to only $3500 left on her student loan. She gave a chuckle and said that she has forgotten almost everything she learned in college. I told her that was alright...

Debt is a prison and you don’t get out of jail until your creditors are paid off. Even if you don’t feel like you are in prison debt still narrows your range of choices and options. You may be just to...

Short answer = Yes. Let’s start with the basics first though. A US savings bond is note representing a US government debt. The government agrees to pay back the money you give them in exchange for interest paid to the bondholder...

This is a guest post by Trisha Wagner. Trisha is a freelance writer for DepositAccounts.com, where you can compare rates from dozens of banks in one place. Trisha writes regularly on the topics of personal finance and saving money. Credit card...

With a name like “Debt Destroyer” it’s kinda implied that I’m spending my waking hours destroying debt. I wish that was the case. But I have to admit that I spend much more time watching “Arrested Development” on DVD, than I...

“I can pay all my bills each month, I am doing well.” In a world of leased BMWs, credit cards galore, no interest credit offers, and high standards of living, what does it really mean to ‘live within your means’? We...

According to the local public radio station, South Dakota students carry the highest debt load in the nation. I was shocked to hear this for a couple of reasons: South Dakota Universities (public ones) are very affordable. For example, I’m currently...