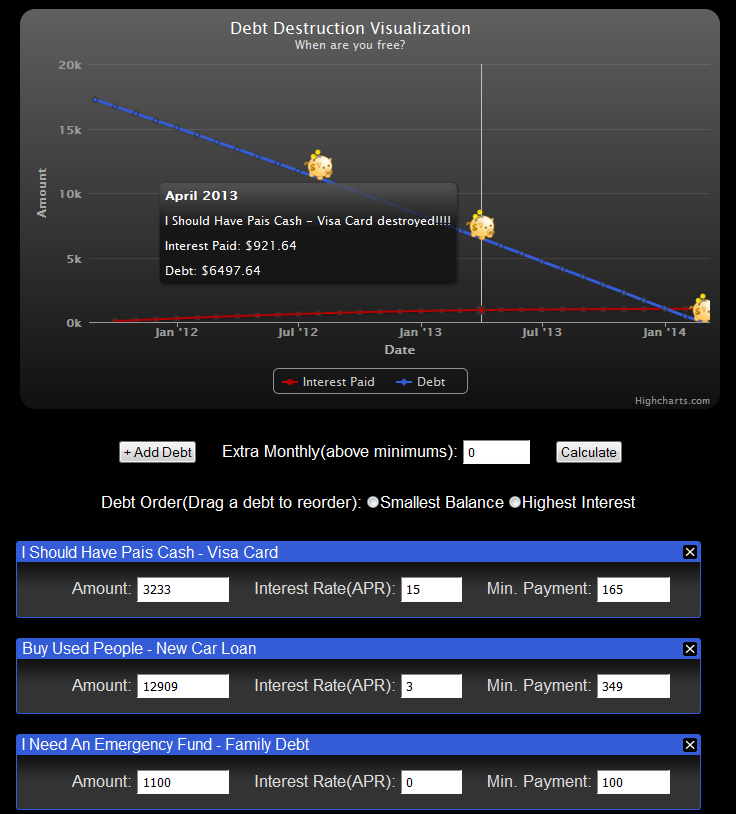

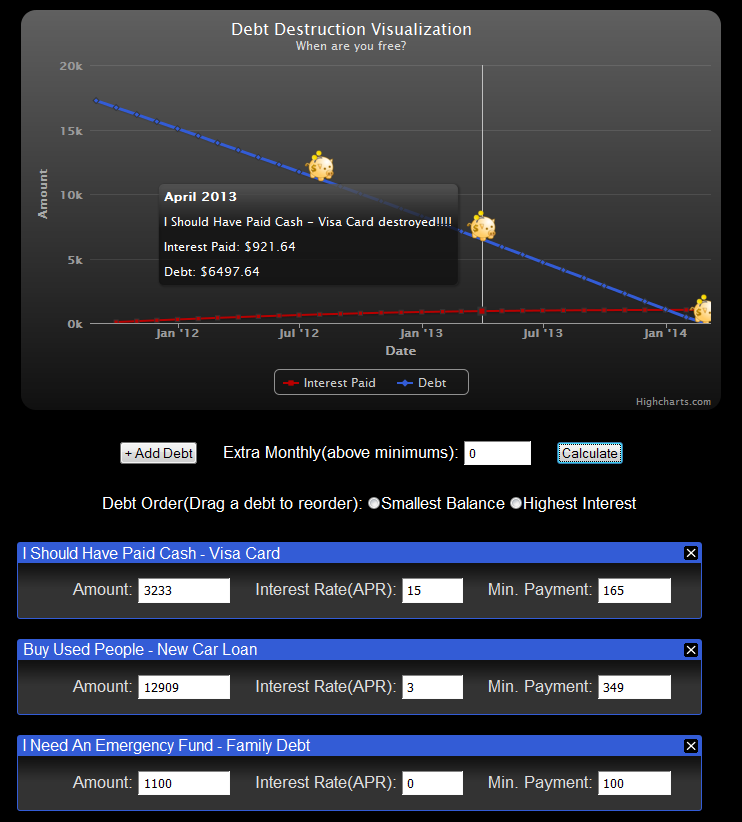

The first release of the online debt calculator is ready for users. The idea is that you don’t need to download a debt reduction spreadsheet or some external program, you can visualize your debt destruction right in your web browser. Debts...

An alpha version is ready of the debt reduction calculator is ready. We will be adding features as the feedback rolls in, so feel free to check it out and leave some suggestions by clicking the “Feedback” tab. The calculator does...

I procrastinated filling taxes this year again…no big deal. Late filing seems to be common practice for those of us who usually owe money each year. The pain came when I received word that we need to file for extension and...

The title is over the top, but I am pretty excited. I can’t call The Happy Rock revitalized until I actually start posting and investing in the community again, but that is my honest desire. The blog has been languishing for...

With mortgage interest rates at amazing lows, I (Ed) figured now is the time for 15 year fixed rate refinance: I have a 30 year fixed rate mortgage with about 23 years and ~$156,000 left. With the 15 year fixed...

This post is about a book that was recommended to my wife called “Pick Another Check-out Lane, Honey(Affiliate Link)“. The two authors cover their ingenious couponing method from soup to nuts. My wife has just begun using this method and with...

Josh Clark invented a running program called Couch to 5k. While, I realize that this program has existed since 1996, it maybe new to you as it is to me. His training system aims to take the couch potato and slowly(and...

The following is a guest post by a dear friend Ed(@ed_bruner) who is just months away from finally getting out from under $40,000+ in debt. Use cash to plug up the holes I assume every family budget has holes in it. ...

The following is a guest post by a dear friend and colleague Ed who is just months away from finally getting out from under $40,000+ in debt. Give him a warm welcome in the comments or a shout on twitter(@ed_bruner): The...

I have been listening and reading through A Million Miles in a Thousand Years: What I Learned While Editing My Life(affilaite link), and in it Donald Miller provides a very simple framework for thinking about your life: your life is a...